In a world where financial security and retirement planning are hot-button topics, the recent announcement by the Social Security Administration brings a breath of fresh air. On October 12th, 2023, the administration revealed that Social Security benefits will increase by 3.2% in 2024, offering much-needed relief to millions of beneficiaries. A beneficiary is a person or entity designated to receive the benefits of property owned by someone else. This annual cost-of-living adjustment (COLA) is a promising step toward helping retirees maintain their financial footing amidst inflation.

Moderating Inflation And 2024 COLA

The 3.2% increase projected for 2024 might appear modest compared to the impressive 8.7 percent jump in 2023 or the 5.9 percent boost in 2022. However, it’s important to recognize that this change is not in isolation but rather a reflection of moderating inflation. The COLA announcement closely follows the release of the latest Consumer Price Index (CPI) report, which found that inflation has increased year-over-year. While inflation remains relatively high, it’s notably lower than the 40-year high of 9.1% experienced last June.

What This Means

The increase in Social Security benefits is expected to impact the lives of 66 million beneficiaries. On average, Social Security retirement benefits will rise by approximately $50 per month, effective in January 2024. The average monthly retirement benefit for workers will increase from $1,848 to $1,907. However, 7.5 million Supplemental Security Income (SSI) beneficiaries will witness the increase in their December checks. This is particularly beneficial for those who rely on Social Security and SSI benefits, offering immediate relief to their cost of living.

Wage Cap For 2024

The Social Security Administration also announced the 2024 wage cap. The maximum amount of earnings subject to the Social Security tax, also known as the taxable maximum, will rise to $168,600, marking a 5% increase from the previous year’s cap of $160,200. This adjustment is crucial as it ensures that the tax base keeps pace with the growth in earnings and cost of living.

Impact On Retirees And Beyond

The importance of this annual benefit adjustment cannot be understated, especially in the context of an aging population and rising living costs. Retirees can now breathe a little easier knowing they will soon receive an increase in their Social Security checks to combat the rising prices. Older Americans, who have been feeling the pinch when buying groceries and paying for gas, can now look forward to a bit of financial relief.

Partner With GMS!

In a world where the financial landscape is ever-shifting, a crucial player takes center stage – a professional employer organization (PEO). Think of it as a strategic partner, working behind the scenes to ensure that businesses can seamlessly extend the benefits of Social Security to their employees. PEOs like GMS serve as a partner, navigating the intricate web of payroll management, tax compliance, and regulatory complexities, empowering businesses to optimize the benefits offered to their workforce. In a world where every dollar carries profound significance, GMS becomes the key player that connects businesses and their employees to financial stability. Contact us today to learn more.

Social Security is the biggest program funded by payroll taxes paid by both workers and employers, along with being the largest source of retirement income for most older Americans. Some think that this could be tied with increases in healthcare and housing costs. The price of prescription drugs has also gone up exponentially.

Ensuring that you have the most up-to-date legislation for your payroll can be a heavy burden that requires significant time and effort. As your trusted payroll partner, GMS can automate the process and help ensure you are compliant with all federal, state, and local regulations.

When you own a small business, you have several responsibilities that you need to oversee throughout the year. Payroll tax management is one of the more notable obligations that are on your plate. Unfortunately, it’s not necessarily obvious how to estimate payroll taxes for a small business.

While it’s not the most enjoyable job, it’s critical that you calculate payroll taxes correctly. Every employer must withhold payroll taxes from each paycheck, so proper handling of these deductions is important to both your employees and the government. This responsibility is a lot of pressure for a small business owner who isn’t familiar with how to withhold payroll taxes. That’s why we’ve put together a breakdown of how to calculate payroll taxes for your small business.

What Payroll Taxes Do Employers Pay?

Payroll taxes are one part of what the IRS considers as employment taxes. The term “employment taxes” actually refers to a variety of taxes that are directly connected to your employees. These taxes include:

Federal and state income taxes

Federal Insurance Contribution Act (FICA) taxes

Federal Unemployment Tax Act (FUTA) taxes

Additional Medicare tax

Self-employment tax

While some people confuse payroll taxes with income tax, the term “payroll taxes” specifically refers to FICA taxes. These FICA taxes are made up of a combination of Social Security and Medicare taxes, both of which are deducted from employee paychecks to fund their respective programs. Altogether, FICA taxes account for a total flat rate of 7.65 percent that’s split between Social Security and Medicare.

These taxes are deducted from employee paychecks, but employees aren’t the only people who contribute these percentages to Social Security and Medicare. Both employees and employers are responsible for paying them, and the employer payroll tax percentage is the same as what employees owe. As such, your business needs to match the flat percentage deducted from each paycheck.

How to Calculate FICA Taxes

The bad news about calculating payroll taxes is that you’re going to have to do some math. The good news is that the math for calculating FICA taxes is much easier than estimating federal income taxes.

The reason why FICA taxes are much more manageable to calculate is that they’re flat percentages. As of 2021, the combined FICA tax rate is 7.65 percent of an employee’s gross pay. That rate is split into the following percentages:

Social Security tax – 6.2 percent

Medicare tax – 1.45 percent

Of course, payroll deductions aren’t always that easy. There are a couple of exceptions to the base rates that can affect your calculations for both Social Security and Medicare taxes if an employee makes more than a certain wage threshold.

Calculating Social Security taxes

In general, calculating Social Security taxes is straightforward – just multiply an employee’s gross pay by 6.2 percent. The resulting number should be deducted from an employee’s paychecks and matched by the employer. However, there is an annual limit to how much employees and employers contribute to Social Security taxes.

Every year, the Social Security Administration sets a wage base for Social Security taxes. Essentially, employers and employees only have to pay these taxes up to a certain dollar amount. The taxable maximum is set at $142,800 for 2021, which means that Social Security taxes only count toward the first $142,800 an employee makes in a year. For example, an employee who makes $150,000 wouldn’t pay Social Security taxes on the final $7,200 in gross pay.

Additional Medicare tax

As with Social Security taxes, there are certain wage thresholds that will impact your exact calculations. Unlike Social Security, these thresholds can mean that individuals pay more in Medicare taxes.

There are no annual Medicare tax limits. Instead, employees who earn more than certain amounts have to pay an additional Medicare tax rate of 0.9 percent. Those wage thresholds are:

$200,000 for employees who are single

$250,000 for a married employee who files jointly

$125,000 for employees who are married, but file separately

It’s important to note that the additional Medicare tax only applies to wages earned above the set thresholds. For example, an employee who is single and earns $250,000 would owe 1.45 percent on the first $200,000 and a combined 2.35 percent on the subsequent $50,000.

Another key detail is that employers are not required to match any additional 0.9 percent contributions. Instead, they would only contribute the standard 1.45 percent. However, employers should still withhold the additional 0.9 percent Medicare tax from employee paychecks. Employees should also file Form 8959 if they meet the requirements for additional Medicare tax.

Payroll Tax Deductions Examples

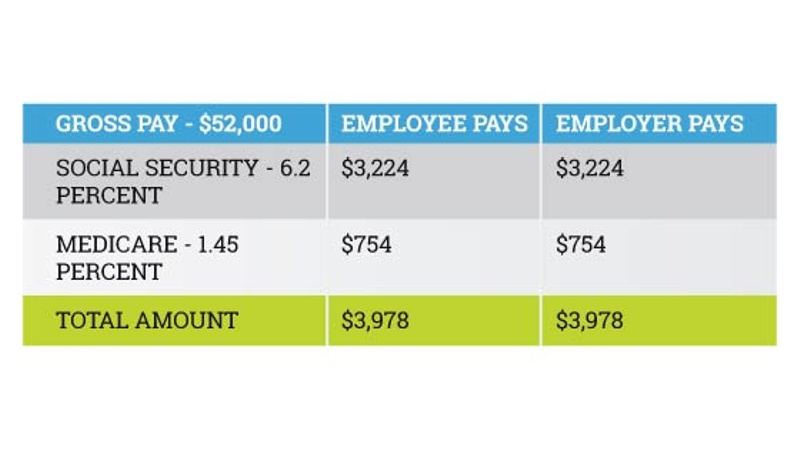

Instructions on FICA tax calculations are nice, but sometimes it’s best to see an example on how to break down these calculations. Let’s start by assuming you have an employee who makes $52,000 in gross pay a year. Here’s a quick breakdown of the annual payroll tax responsibilities for that employee.

While the numbers above give you an idea of how much both you and your employee will pay in annual payroll taxes, you’ll also need to determine deductions on a per-paycheck basis. Identifying per-paycheck tax deductions will allow you to withhold the right amount from each employee’s paycheck while helping you keep track of what you owe when it’s time to pay the employer portion of payroll taxes.

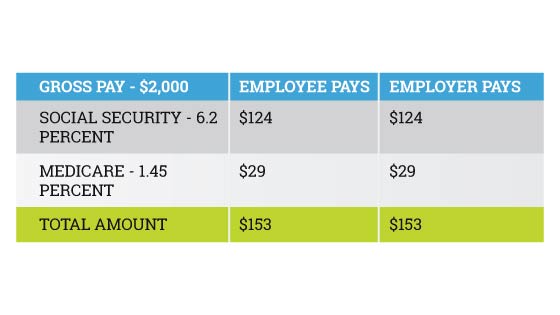

Determining deductions on a per-paycheck basis depends on your pay frequency. There are multiple pay period options depending on your location – weekly, biweekly, semimonthly, and monthly are all fairly standard. You’ll need to divide an employee’s annual gross pay by the number of pay periods in a year and apply the appropriate FICA tax percentages to that individual paycheck. Here’s a breakdown of that same $52,000 employee on a biweekly pay period.

How to Pay the Employer Portion of Payroll Taxes

Calculating and withholding FICA taxes is just one part of the process. As an employer, you still need to pay those withheld and matched taxes to the IRS.

Employers can report and pay FICA taxes through their Electronic Federal Tax Payment System (EFTPS) account. Employers must send regular payroll tax reports to the IRS through Form 941. The due dates for Form 941 are the final day of each quarter (April 30, July 31, Oct. 31, Jan. 31).

In terms of depositing payroll taxes, the frequency depends on how much you paid in the past year. Businesses that reported more than $50,000 in federal taxes on average must deposit taxes semiweekly. Businesses that pay on a monthly business owe these taxes by the 15th of the following month.

New businesses or businesses that reported less than $50,000 on average only have to pay federal taxes on a monthly basis. The due dates for these payments depend on your paydays. If paychecks are due Wednesday through Friday, you need to deposit taxes by the following Wednesday. If payday falls on Saturday through Tuesday, those same taxes are due by the following Friday.

Take the Pain out of Payroll Management

Even if you have a grasp on calculating payroll taxes, you still have a lot of work to do. Managing payroll and tax filings can be one of the most time-consuming and challenging tasks there is for a small business owner. That’s why employers turn to GMS for payroll administration.

When you work with GMS, you get to stop worrying about the ever-changing nature of payroll tax management and start spending time growing your business. Contact GMS today about how we can help you take control of your critical HR functions.